The Analyst View

You can’t eat money

You can’t eat money

It is broadly accepted that the largest economies in the world are driven by consumer spending. The consumer driven society prioritizes the consumption of goods and services over production, and the economic engines for these countries spin best when citizens are purchasing goods, enjoying services, and spending instead of saving. Companies in a consumption economy seek to lower their costs by building a global network of suppliers, and gain market share by offering products of a similar quality to the competition at a lower price. Often this comes at the expense of domestic jobs and wages. This view of the world, sometimes called Keynesian economics, is a hotly debated concept that believes production is not an essential component for economic prosperity as long as low prices on goods generates a higher standard of living.

The poster child for this style of economy is, of course, the United States. The world’s largest economy since 1871, the United States just posted record growth of 33% annualized for the third quarter of 2020 according to the Bureau of Economic Analysis (BEA). The $1.64 trillion increase of current dollar GDP to $21.26 trillion is the largest single quarter of economic growth on record and approximately twice the prior record set during the first quarter of 1950. The rebound in the economy in the third quarter allowed the United States to recover two thirds of the economic output lost in the first half of the year.

Haiku

Whether you call it

Main street, High Street,

or just home

The stores are closing

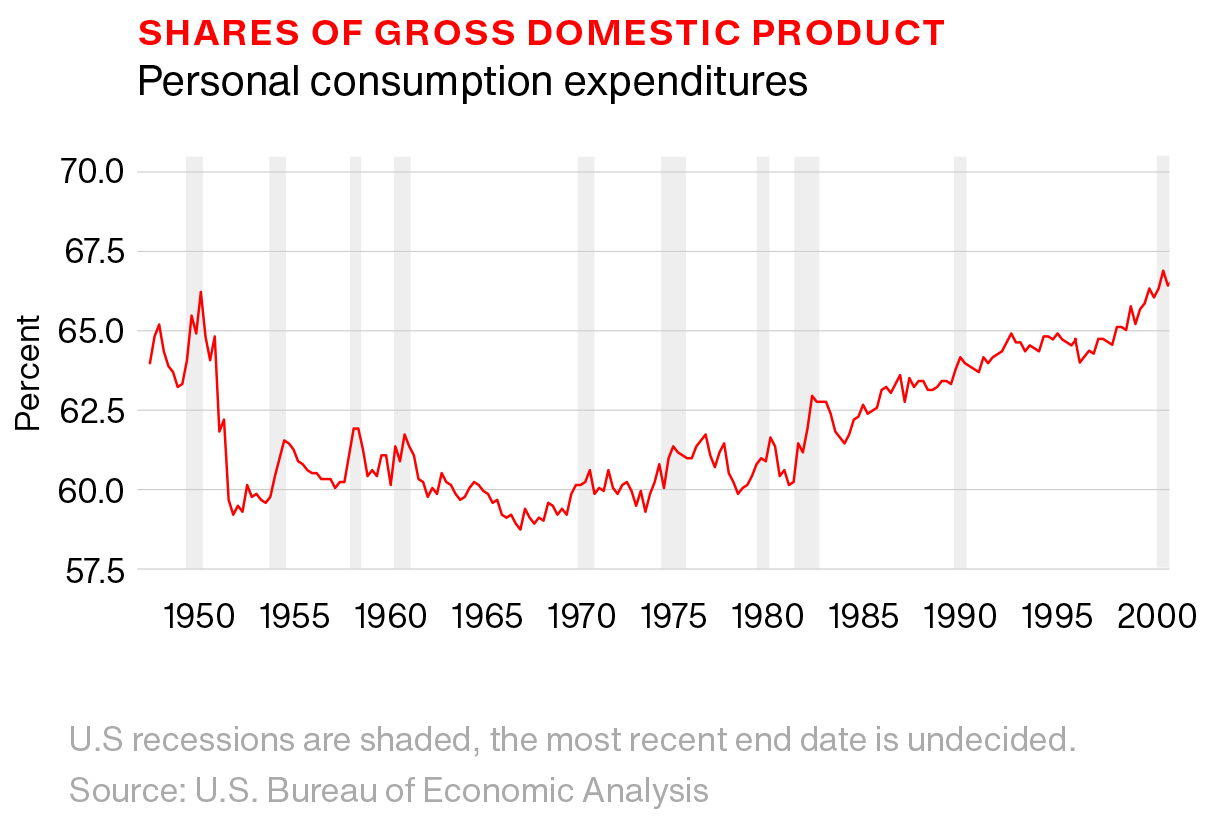

Driving this remarkable rebound in growth is the U.S. consumer, always willing to spend. The Federal Reserve bank of St. Louis which tracks personal consumption expenditures as a share of gross domestic product, showed that consumer spending accounted for 68% of U.S gross domestic spending, a total of $14.3 trillion spent. On an annualized basis, spending increased by 40.7% in the third quarter when compared to the second quarter, according to the BEA. To see how important the consumer is to the United States economy, just look at the chart below showing the steady climb of consumer spending as a percent of the overall economy. The push to get consumers to spend is also supported by the Federal Reserve that has set a base interest rate of 0%, essentially creating a system that causes savers to lose purchase power as time advances when adjusting for inflation. So how is all this money spent?

Clearly there is a massive shift in consumer behavior to online commerce channels that was already underway before the 2020 pandemic. The decimation of retail stores can be seen when a record 9,500 locations closed in the United States in 2019, up a startling 64% from the 5,844 businesses that closed in 2018 according to Coresight Research. Estimates for 2020 bleakly show up to 25,000 businesses closing. Many of these locations are located in shopping malls, the center of the retail apocalypse. Even more bleakly, an increasing number of retailers are choosing to head directly into liquidation rather than pursue an attempt to restructure and continue operations. In the United Kingdom, a common refrain is the disappearance of High Street and the data supports this thesis with record business closings in the first half of 2020. The 6,001 net store closures during that time period is almost twice the 3,509 net closings in the same time period of 2019. The British Retail Consortium has labeled the situation “a nightmare before Christmas” and cited that retail foot traffic is down by as much as 75% from 2019.

Those familiar with Interbrand’s canon of work may have encountered the concept of Iconic Moves. It’s a framework of thinking that includes a commitment to change that is materially above the rest of an industry, change that is driven from the inside out. Picture the current state of the retail market. An industry that has had to grow a decade’s worth of skills in 2020 to survive higher operating costs, government intervention, and a customer base that is abandoning them to shop online. It’s clear why some businesses decided to resolve their woes by heading directly to liquidation. After managing the daunting industry turmoil of recent years caused by changing consumer patterns, when the pandemic challenges of 2020 arrived, it’s understandable that certain business owners called it quits. It is a simpler task to pursue a home garden and tend to the backyard chickens.

Gary Hamel, an influential expert on business strategy, is quoted as saying “inventing an innovative business model is often mostly a matter of serendipity.” When taken to the core, all business models run on two levers: pricing and costs. The art is to correctly determine, as Peter Drucker eloquently stated in his theory of the business, the set of “assumptions about what a company gets paid for.”

It was 1999 when Amazon as a company first topped $1 billion in sales, and internet enabled commerce was a mere 0.5% of total retail sales in the United States. Amazon’s operating expense was 3x larger than its gross profit that year, and the company suffered a net loss of 44 cents for every dollar of revenue. CEO Jeff Bezos made clear to investors in his first letter to shareholders printed in 1997, and reprinted every year since, that the company was going to be focused on “bold rather than timid investment decisions” with a “focus relentlessly on our customers.” The company was in pursuit of a long term victory as the CEO stated then “this is Day 1 for the Internet and, if we execute well, for Amazon.com… online commerce saves customers money and precious time.”

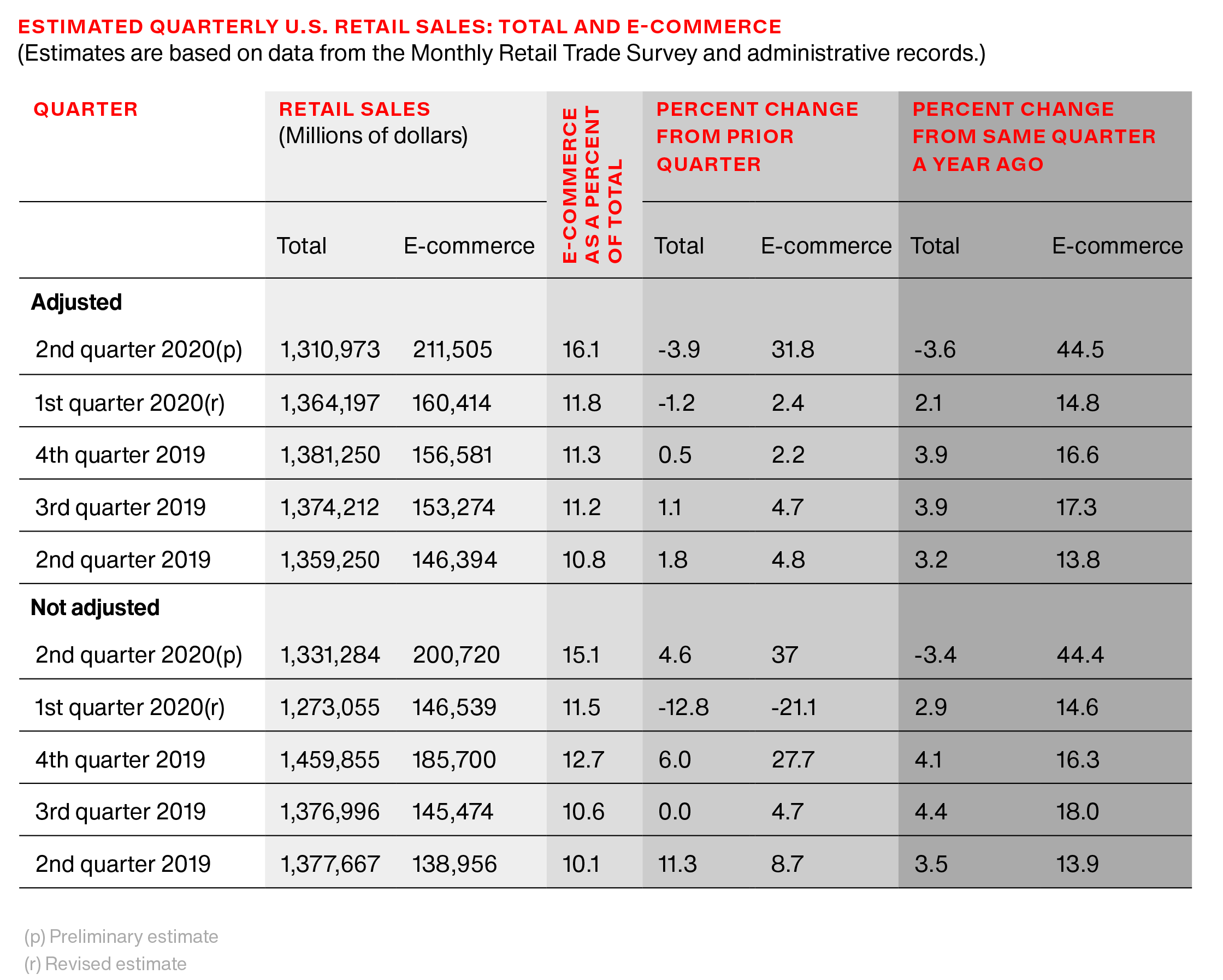

In the two decades that have passed, e-commerce has risen to 16.1% of total retail sales in the United States according to the latest data from the U.S. Department of Commerce. While the data shows that total retail sales declined 3.6% from the prior year, growth in e-commerce registered at 44.5%, sharply eclipsing the typical growth rates of 15-17% seen in prior years.

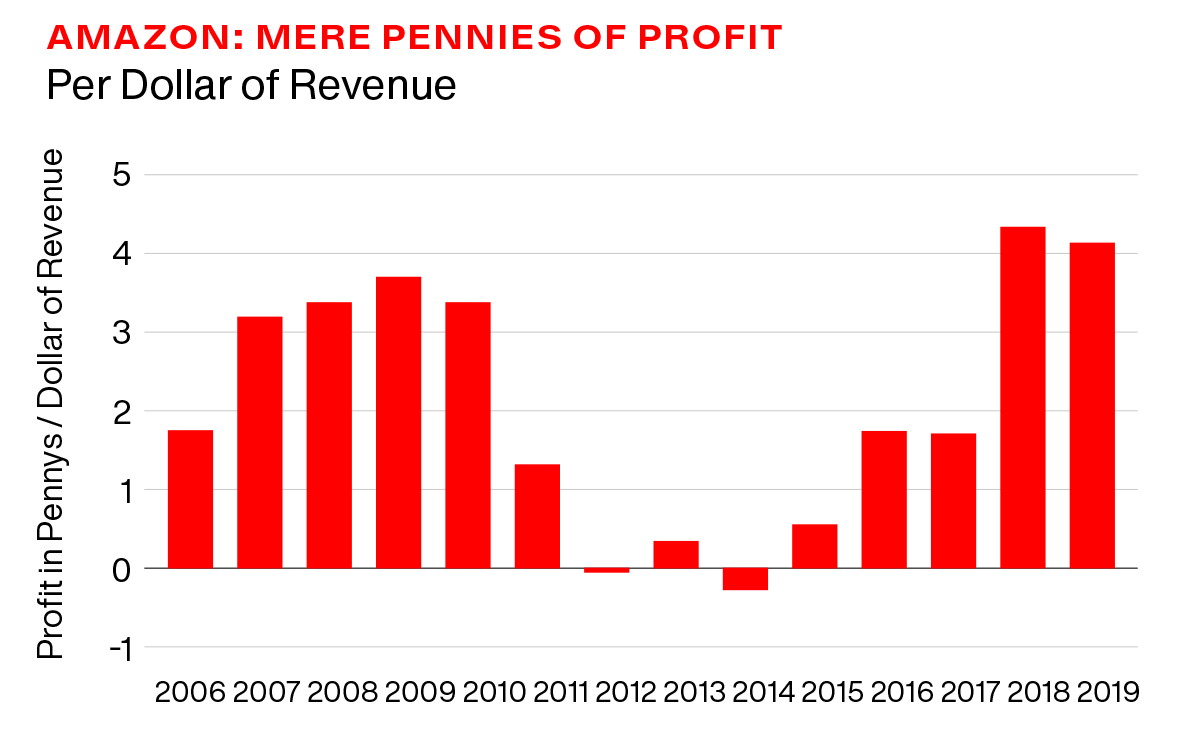

Since its IPO in 1997 at a split adjusted share price of $1.50, management of Amazon has stayed true to its North Star. By keeping its focus on satisfied customers and constantly reinvesting free cash flow back into the business, the financial markets have rewarded investors with a stock price of well over $3000 per share. This is an ROI of over 200,000% (not a typo) and an annual return during the 23.5 years since the IPO of 38% per year. Competition has learned that it is difficult to battle with a company that is allocating decades of time for its dominance and excellence to permeate the market before generating profit leverage. Today Amazon boasts over 150 million subscribers to its Prime service, and is on track to generate $375 billion in turnover in 2020 according to Interbrand research estimates. Amazon is in the forefront of utilizing both robotics and artificial intelligence to improve efficiency for customers and remove costs. The company acquired Kiva Systems in 2012, now called Amazon Robotics, to drive automation of the warehouse picking and packing process. Amazon let the contracts that Kiva had with other customers expire, and is now the sole user of the technology. The Associated Press reported this year that Amazon uses over 200,000 robots, up from a reported 100,000 robots working in Amazon warehouses in 2017. Even with the robots, the company is a relentless hiring machine adding over 250,000 employees since the start of the pandemic in February 2020 to add fulfillment capacity. The most recent headcount for the company stands at 1,125,300, the first time the company has crossed the million employee mark, and a 50% growth rate in employees year-over-year. These workers in Amazon fulfillment centers share space with a multitude of different robots, a compelling dance of man and machine. The company also leans heavily on its artificial intelligence to recommend products. Piecing together a product graph from machine learnings based on historical purchase grouping, browsing history, and buying history, the company is reported to generate as much as 35% of its revenue from its AI driven product recommendation engine.

While it’s laughable now, it’s entirely possible that Sears, Roebuck, and Co. could be the company still holding the retail crown instead of Amazon. It’s a similar story. Sears mail order growth came from rural consumers seeking an alternative to expensive general stores that lacked scale and buying power. Sears offered a deep selection of products published via its “Consumers Guide” catalog that often exceeded 500 pages. The company sold everything, and its catalog declared itself a “Book of Bargains: A Money Saver for Everyone”. Handwritten notes, a money back guarantee that started in 1903, and a slogan that claimed “We Can’t Afford to Lose a Customer” showcased the laser focus on customer service and quality.

The firm went public via Goldman Sachs in 1906, the largest retail public offering ever at the time, and opened a 40 acre logistics center in Chicago – the middle of the United States – that was lauded for its efficiency. When the company started opening stores across the country in the 1920s, it was unwittingly planting the seeds for its eventual downfall.

Noted academic Clayton Christensen touches on this point with his statement that “the reason why it is so difficult for existing firms to capitalize on disruptive innovations is that their processes and their business model that make them good at the existing business actually make them bad at competing for the disruption.” In other words, keeping up with the times is not so easy.

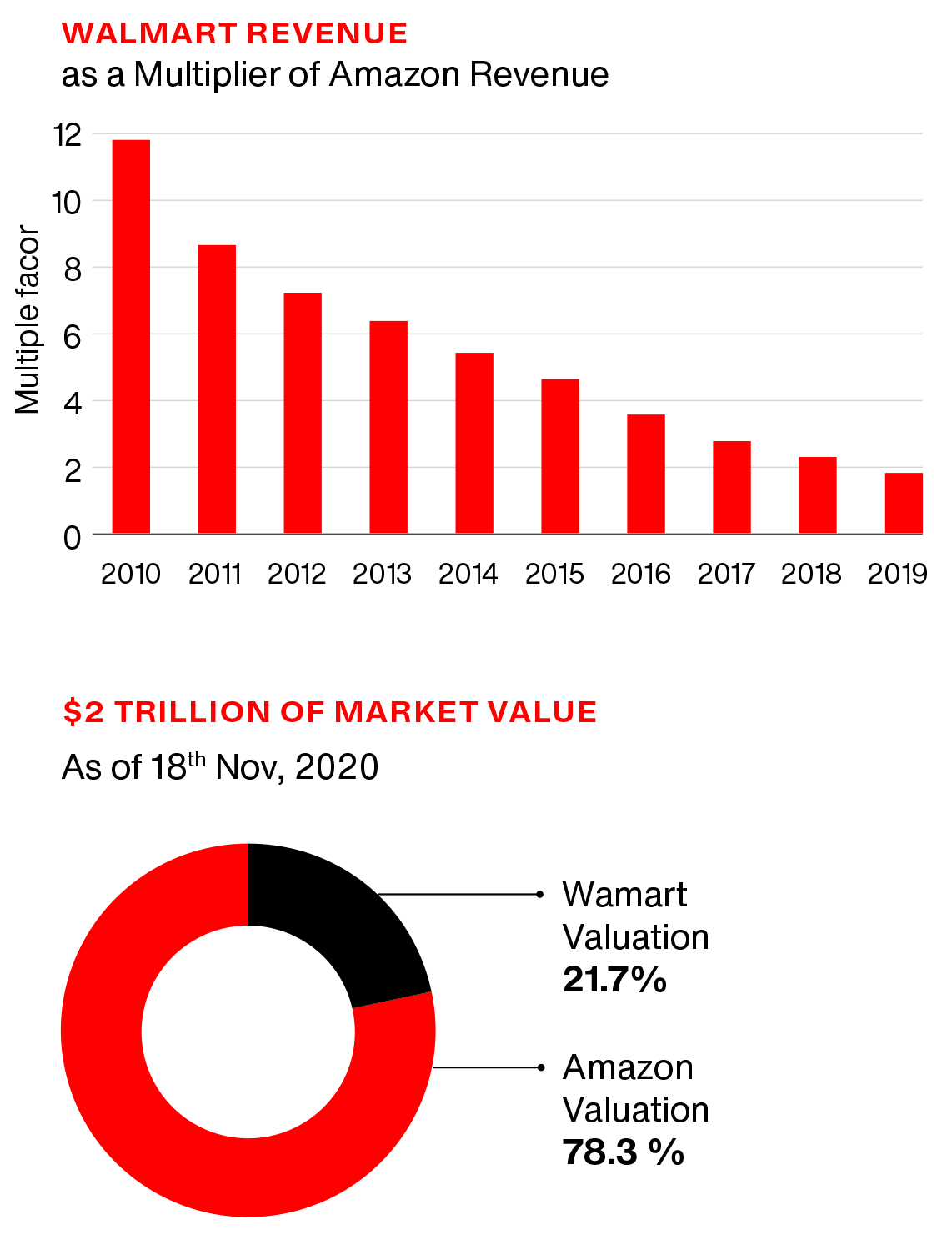

Which brings us to Walmart. The company that will once again generate more revenue than Amazon in 2020. A company that has 265 million customers each week and a global footprint of over 11,000 stores in 27 countries. A company that has 50 years of supply chain excellence, embraces technology, offers a wide selection and low prices. It is the largest business by revenue in the world, it has been the largest business by revenue in the United States for over two decades, and is thought to be the source of demise for small businesses across the globe.

Walmart is also a company that is in the middle of a major overhaul. Despite its clear heft, its leadership position is eroding.

Shown another way, one can see the steady erosion of Walmart’s leadership, from booking 12x the turnover of Amazon in 2010 to booking less than 2x Amazon revenue in 2019. Interbrand research estimates that Amazon will eclipse Walmart revenue by 2024.

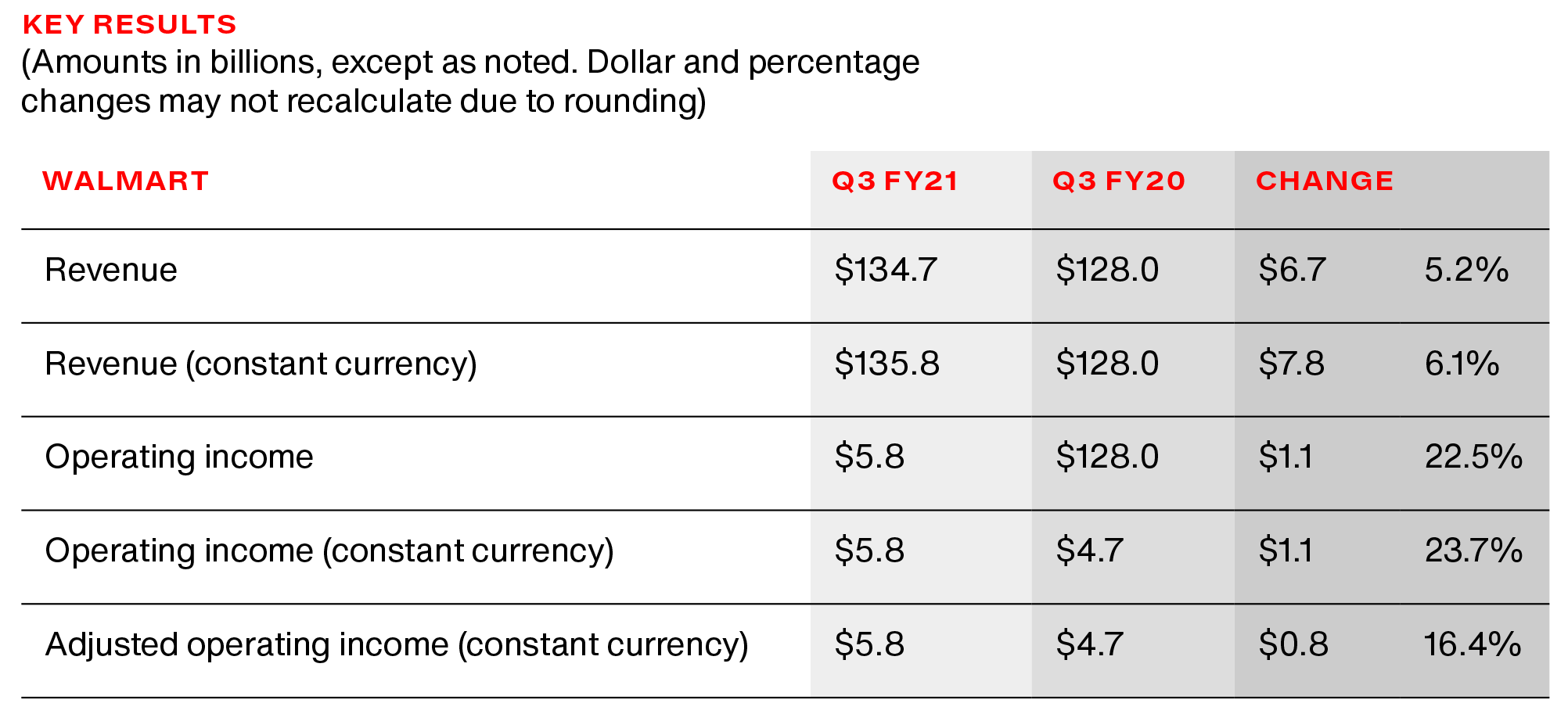

There is a reason that investors value the business of Amazon three times what they value Walmart. Even though Walmart’s September quarter results materially exceeded investors expectations with revenue growth 5.2% and an increase of average purchase size by 24%, the thinking is that browsing in stores is an outdated concept.

To solve its dilemma, Walmart is taking an approach to redesign its store with more open space, larger signage and contactless payments. The cues for the store redesign come from the interior of airports, using best in class navigation techniques to move volumes of customers where they need to go efficiently. There is another key component of the redesign that is critical for Walmart’s future. From the company press release: “As customers enter the store, they are greeted with clean, colorful iconography and a store directory that encourages them to download and use the Walmart app while they shop”.

By offering in-store navigation via the app, Walmart creates an incentive for its customers to download and engage with their mobile phone, both in and outside of the store. As the company says “a transformational journey… reimagining ways to create seamless omni-shopping experiences that save our customers time and inspire them whether in-store, online or via mobile.” This strategy may allow the company to turn its large footprint of stores into an asset, not a dead weight, as the dense store network can play a larger role in its e-commerce future. Walmart’s existing footprint is structured so that there is already a store within ten miles of 90% of the U.S. population according to the company. These stores are served by a network of 150 distribution centers, with each center supporting 90-100 stores in a 150 mile radius. This means that the inventory consumers are seeking is already forward deployed to its stores and within 10 miles of the customer, an advantage that the company needs to better exploit.

Walmart also has an inherent advantage with consumer packaged goods (CPG). A highly competitive sector because of saturation and low switching costs, Walmart is able to better offer the edge that brands fight for, including shelf space and signage. A recent price comparison study also shows that Walmart has the best prices on home goods (detergent, soap, toothpastes) compared to Amazon and Target, although the price differential was generally less than 2%. The thinner margins of CPG also make the products well suited for omnichannel commerce, with the ease of mobile and e-ordering, and the cost advantage of not shipping often weighty products.

Mastercard eloquently stated “payment is only the final step in a customer journey that should be an enabler and not a barrier to the completion of a purchase. Both consumers and retailers demand simplicity, seamlessness and safety”. The company lays out the challenges facing retailers in breaking down the siloed channels of payments that can happen between point of sale and in-app purchasing solutions. The payment goal for retailers is three fold:

The last point is important because this is the area where retailers can close the loop between the various expressions of interest in a product that a customer may express in an omnichannel environment. This includes looking at the product online and purchasing in the store, seeing the product in store and purchasing online, or other combinations.

Here it is worth a look into a product offering that is not often included in a discussion of the retail sector. This is the category of products with the special price of zero. Consider Google, a company that offers 9 products that have over one billion users each. These products include Search, YouTube, Maps, Gmail, Drive, Photos, Play, and Android.

All these products are offered to its customers for the special price of zero. The company is worth over $1 trillion dollars on the back of these free products. Facebook has over 2.7 billion monthly users of its free products. Both of these companies are pushing into payments as it allows their advertising model to become more efficient by closing the loop on consumer transactions.

Google just announced an extensive revamp of its Google Pay service including a new offering of checking accounts in partnership with major banks. Home assistant devices like Amazon Alexa and Google Nest Mini are increasingly being given away or sold below cost because the value of the data insight and presence in the consumer’s home has a longer and more enduring value than any small one-time profit from the hardware sale. Just like the classic late night TV pitch “Yours Free! Just pay shipping and handling…” we expect to see more innovation in this area as retailers experiment with price in relation to the value of the data that is collected.

“We at BMW do not build cars as consumer objects, just to drive from A to B. We build mobile works of art.” Chris Bangle, Chief of Design, BMW Group 1999-2009

The business cycle moves at different speeds, with acceleration in one part of the world igniting a butterfly effect across the globe. In the current climate, advanced economies see production as holding less value than knowledge and human capital. In the United States, the number of actual, physical buildings used for manufacturing fell below the number of actual, physical buildings used for warehousing in 2001, a clear marker in a time chart that distribution had become more primary than production in the country. It all leads to change, and 2020 has proven to be an accelerant for change that has no compare in recent history. The year has forced people to reassess their consumption and patterns, often due to Government lockdowns. Health concerns compressed technology adoption that may have taken a decade into a three-month time span.

Customers are fundamentally reappraising themselves, questioning how they want to be consumers going forward, if at all, and demanding that brands that serve them follow suit. Brands that desire to stay relevant need to anticipate tomorrow by understanding what people are doing today. It is a reminder that Blockbuster could have been Netflix, Yahoo could have been Google, Oldsmobile could have been Tesla.

To end with another quote from Gary Hamel, “In a world of commoditized knowledge, the returns go to the companies who can produce non-standard knowledge.” It can be as simple as listening closely to your customers.