Thinking

Where’s the Value in Brand Valuation?

Where’s the Value in Brand Valuation?

In October, I was invited to participate in a debate on the merits of brand valuation at the Festival of Marketing in London, during which criticisms were leveled against brand valuation rankings like Interbrand’s Best Global Brands, published annually since 2000 and voted one of the three most influential benchmarking studies by CEOs in a PR Week report. The three criticisms focused on:

1. Variation

2. Denunciation

3. Deviation

Let me tackle each of these fallacies in turn.

This takes issue with the fact that, in some cases, the valuations published by the three consultancies that produce the top brand valuation rankings vary significantly. Take Apple, for example, the number one brand in all of the consultancies’ reports. In 2015, Interbrand’s opinion of the value of the Apple brand was $170 billion. Brand Finance’s valuation was more conservative at $128 billion and Millward Brown’s was more “bullish” at $247 billion. From lowest to highest, the difference in value is 93 percent, or $119 billion.

Large differences, and yes, these are big numbers, but then again, Apple’s entire business is worth around $650 billion, so you’d expect its incredibly strong brand to be a good chunk of that.

Fundamentally, it’s important to remember that brand valuation, like any other valuation, is an educated opinion. It isn’t a price from an actual transaction, but an informed point of view arrived at by evaluating the brand through a particular methodological lens at a specific point in time. There’s absolutely no reason why valuation opinions shouldn’t vary significantly, and we see this all the time in other places.

To illustrate the point, consider a brief story of a shareholder dispute that Interbrand was recently involved in. A blue chip multinational had just sold an online retail business for £950 million. The minority shareholders disputed this value and hired Interbrand and Morgan Stanley to value the business (Morgan Stanley using traditional business valuation techniques, Interbrand through a brand valuation lens). Both of our valuations were a long way north of £950 million. An arbitrator was subsequently appointed, the Big Four accountant Deloitte, who reviewed very detailed submissions from all parties involved.

The end result was that the value of the business was deemed by Deloitte to be £1.5 billion. So, a great success for our client, but to my point above, a very significant difference in opinion on value (of nearly 60 percent), even in a situation where all parties had access to exactly the same data and the valuation received huge levels of scrutiny on all sides.

As another example, let’s consider equity analysts, who follow stock markets and recommend that you should buy or sell specific shares, once again taking the example of Apple, one of the most well researched shares in the world. When we looked at reports in September 2015, the difference between the highest and lowest target share price among the 47 equity analysts covering this stock was 106 percent. In September 2014, when we did the same thing, the difference was 170 percent.

Cue outrage from journalists looking for easy headlines? No, actually, because the people who look at these share price recommendations are financial investors who understand valuation and recognize that relatively small changes in valuation assumptions can have a big impact on values. This is why significant expertise and judgment, in addition to analytical skills, are essential to getting the most out of a valuation exercise.

The second argument was that we, the three consultancies participating in the debate, don’t spend any time criticizing each other’s valuations. Surely, it was argued, if we were so confident in our valuations, we would critique our competitors where we felt they had got things badly wrong.

As I am sure all business leaders would agree, we would prefer to spend our time communicating the benefits and value of our own services than criticizing the competition. Fundamentally, Interbrand’s brand valuation philosophy is about the importance of generating action. While the number itself is useful (for communication and as a baseline), and must be robust, the most important part of the valuation process are the insights generated and the actions taken as a result. Interbrand is working with blue chip brands on multi-year valuation assignments across our global network of offices. We would much rather talk about the value that these clients gain from working with us.

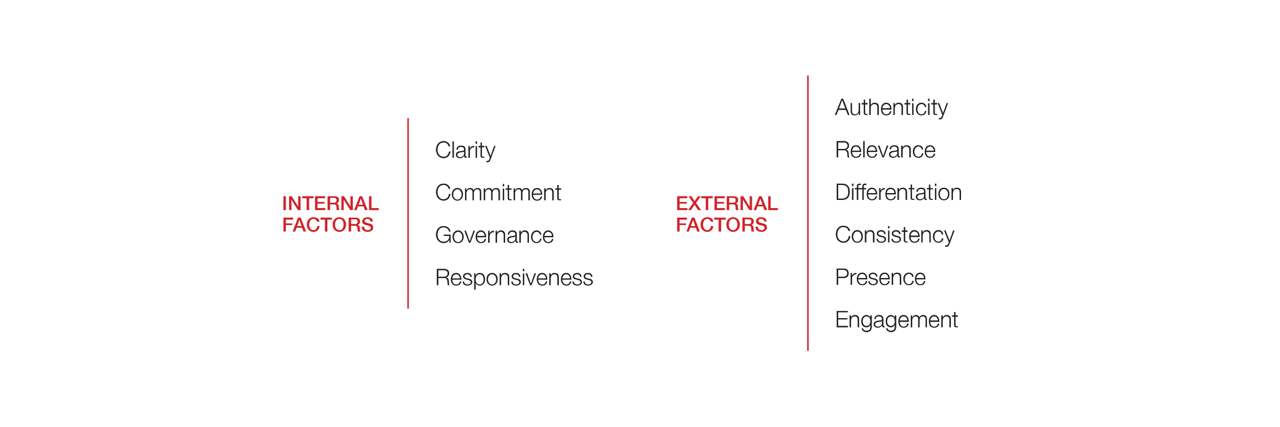

Our Brand Strength framework is our key diagnostic tool. These are the 10 factors that we believe make a strong brand. Internally, we look at everything from Clarity about what the brand stands for to Commitment to delivering the well-defined brand experience. Externally, we look at the brand from the customer perspective, measuring performance on factors like Authenticity, Relevance, and Engagement. We don’t believe that an evaluation of a brand is complete without both internal and external perspectives, and we are the only consultancy to look at both sides of a brand in this way.

We use the Brand Strength framework to first diagnose strengths and weaknesses. We then work with clients to prioritize the key areas to address, leveraging our strategy, experience, and activation disciplines, and generate action plans to strengthen a brand and increase its value.

Interbrand’s proprietary Brand Strength framework:

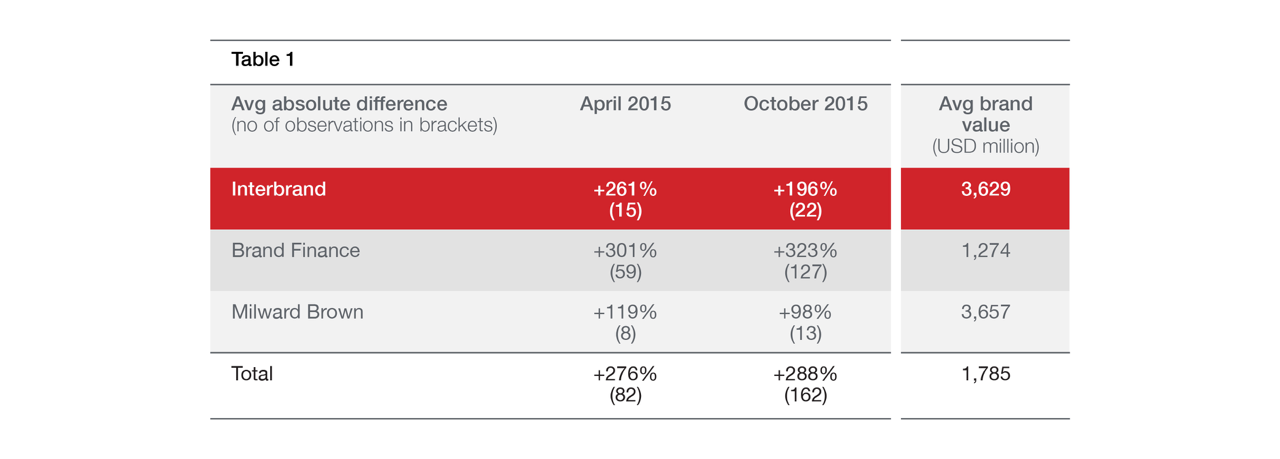

The final discussion point referred to a study conducted by a firm called Markables. Markables has a database of brand values that have been recognized on company balance sheets following acquisitions. The firm cross-matched the brand values from all three consultancies’ published rankings against their own database in order to measure the average deviation for each. Their findings suggested significant differences, reproduced below in the summary table from their report:

In theory, this kind of comparison is an interesting idea, but in practice—unfortunately for Markables—there are a number of reasons why balance sheet values may differ considerably from published rankings. The first I have already addressed above: that it is perfectly reasonable to expect quite significant differences of opinion in the value of a brand, a business, or any other asset.

However, there are specific additional issues with the Markables approach. Let’s take the Interbrand data set (which, by the way, is limited to a statistically insignificant 22 brand values) to illustrate.

My main concern with this study is the assumption being made that the published and balance sheet valuations are conducted based on identical ideas about how the brand will be used in the future. Almost always, Interbrand assumes in its own valuations that the brand will continue to be used forever by the business that runs it. Following an acquisition, however, it is often the case that an acquired brand may be re-branded or discontinued. This happened with two significant valuations within our sample set.

The first was Kabel Deutschland, included in our 2014 Best German Brands. Interbrand’s value of €1.2 billion represented a (relatively conservative) 13 percent of the total Kabel Deutschland business value at the time. However, when Vodafone bought the business for €10.7 billion, it valued the brand at £18 million—less than 0.5 percent of the purchase price![1] The reason for this is very clear when you see that Kabel Deutschland was migrated to the Vodafone brand some time after its acquisition. Clearly, no finance director is going to place a significant value on an asset that he or she would soon have to write off, with negative implications for reported profits and earnings per share.

The same logic applies to the valuation of the Compaq brand by HP in 2002. HP re-branded a significant proportion of the Compaq product range to HP, post acquisition. Assuming that this was planned, then, again, it wouldn’t make sense to attribute too much value to the Compaq brand, only to have to impair or write off that value in the future.

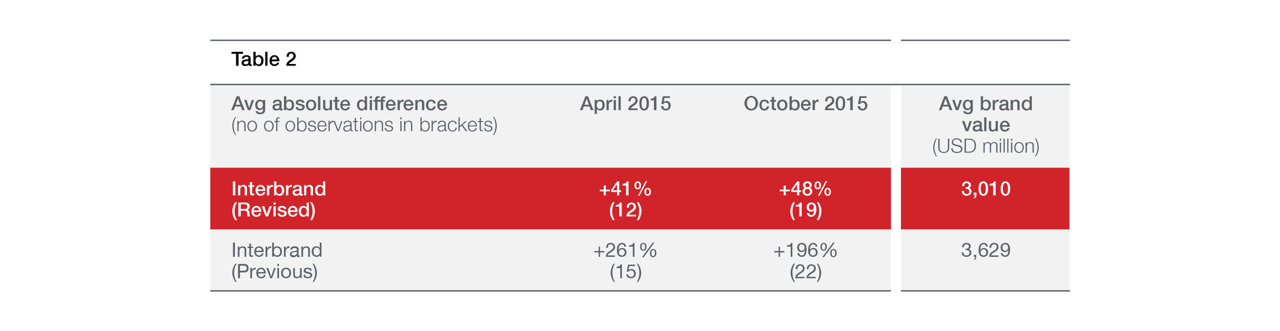

Finally, Markables made an error by including the Korean brand, Korea Express, which Interbrand has never publically valued. Removing these outliers and an erroneous case from the data set reveals a very different looking table:

In fact, when you weigh the deviations in value by size (because it’s much easier to be 100 percent out on a valuation of $1 vs. $2 than a valuation of $100 billion vs. $200 billion), then Interbrand’s deviation falls even further, from 48 percent in the October 2015 data set to 31 percent.

So, although I disagree with the Markables approach in principle, a corrected version of their analysis falls comfortably within the margins for variation that I have already highlighted as reasonable.

The above analysis and commentary above are intended to round out the short debate that we had on the value of brand valuation.

There is more that we, the three brand consultancies, can do to explain why these differences exist, and will no doubt persist. I invite the brand valuation community to work together to shed greater light on the subject.

[1] Figures were reported in these different currencies in the Vodafone 2014 annual report.